Investor Relations

Macroeconomic updates - all news

Cloudy with a chance of hail according to Statistics Iceland

This morning, Statistics Iceland (Statice) published a new economic forecast, its first forecast since WOW air’s bankruptcy. We had eagerly awaited the publication, as our Economic Outlook has been the only official macroeconomic forecast to date that includes WOW air’s bankruptcy. Statice GDP forecast assumes a much smaller economic contraction this year than our forecast, in addition to stronger turnaround in the coming years. Hopefully that will be the case, but we must admit we are doubtful. In our opinion, Statice is too optimistic when it comes to the impact of WOW air’s bankruptcy on exports, unemployment and private consumption. Statice must of course be prudent when publishing forecasts, as government budget is largely based on them. In recent years, this has resulted in forecasts being too pessimistic but, this time around, we are concerned that it will be quite the opposite.

Following is a brief comparison of Statice forecast and Arion Research’s Economic Outlook.

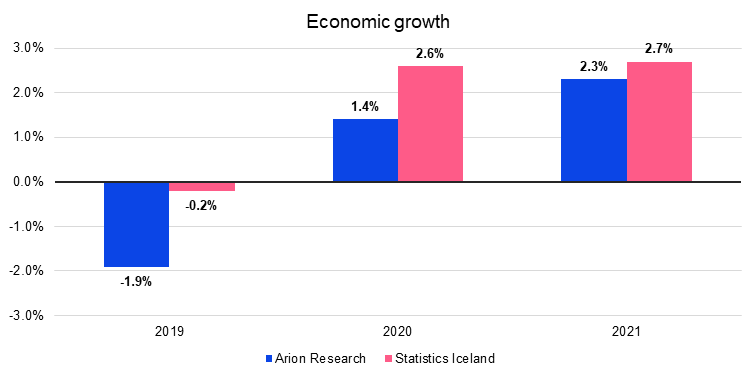

GDP: Statice forecasts a slight economic contraction this year, or 0.2%, compared to Arion Research’s more pessimistic forecast of 1.9% contraction. Furthermore, Statice expects the economy to quickly bounce back, climbing to 2.6% GDP growth as soon as 2020. The main differences between these forecasts is the development of external trade and private consumption.

Sources: Statistics Iceland, Arion Research

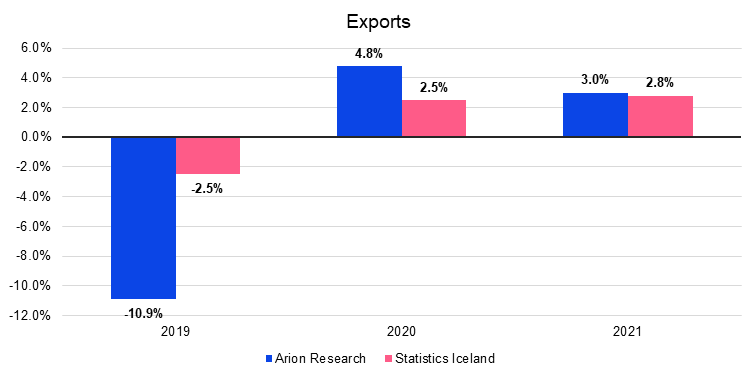

Exports: Statice forecasts a 2.5% contraction in exports this year due to a decline in tourism and supply shock in marine exports. It’s noteworthy in our opinion that the decline is not greater given the fact that the two largest export sectors are hard-pressed. Statice doesn’t publish a breakdown of exports, which means we have to try to fill in the blanks. First off, according Statice report, a considerable contraction in marine exports is forecasted as capelin quotas were not released for this year. Last year alone export value of capelin amounted to 18 bn. ISK, or 0.6% of GDP.

What about tourism? If we take out the export value of capelin and use Isavia’s tourist arrival forecast, which assumes a 2.4% decrease, back-of-the-envelope calculations result in an export forecast that is very similar to Statice forecast. So is Statice basing its economic forecast on an outdated tourist arrival forecast, a forecast that nota bene is built around two operating Icelandic airlines? Or is it expecting other airlines to pick up the slack, despite Icelandair having a hard time growing due to grounding of nine Boeing MAX 737´s? Regardless, both of the assumptions are questionable in our opinion. Hence, it is our view that Statice is too optimistic when it comes to exports.

Sources: Statistics Iceland, Arion Research

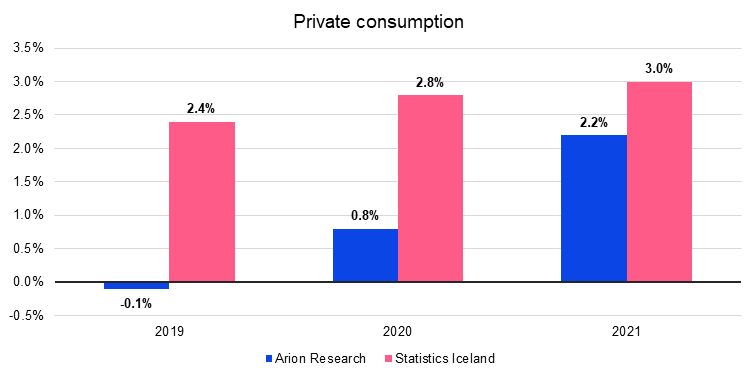

Private consumption: Statice expects decent private consumption growth this year, or 2.4%. The report states that “It is possible that the first few months have been characterized by precautionary savings due to uncertainty surrounding collective wage negotiations in the labor market.“ We expect unemployment to climb higher this year than Statice, to 4.4% compared to 3.7%. It appears that rising unemployment plays a greater role in our private consumption forecast. Admittedly, it must be said that the risk in our forecast is upwards. We might be underestimating private consumption growth, for example because our forecast was based on incorrect payment card turnover figures. After the CBI corrected the numbers, payment card turnover growth proved to be more resilient than previous numbers had indicated. However, a 2.4% private consumption growth is pretty hefty.

Sources: Statistics Iceland, Arion Research

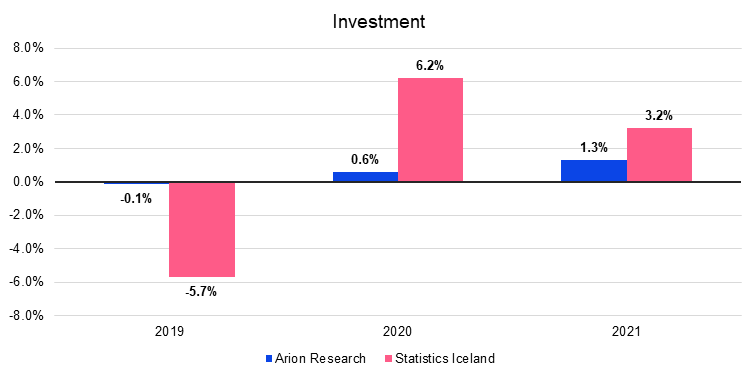

Investment: There is quite some difference between the investment forecasts, mainly due to different outlooks on business investment. While Statice expects business investment to contract by 10% this year our forecast only assumes a 4% contraction. Statice expects a slight contraction in regular business investment and investment in heavy industry, while we expect a slight growth. The forecasts appears to be in unison when it comes to ships and aircrafts, a considerable contraction is foreseen.

Housing investment is similar between forecasters, but there is a difference in public investment forecasts, as various government investments have recently been delayed.

Sources: Statistics Iceland, Arion Research

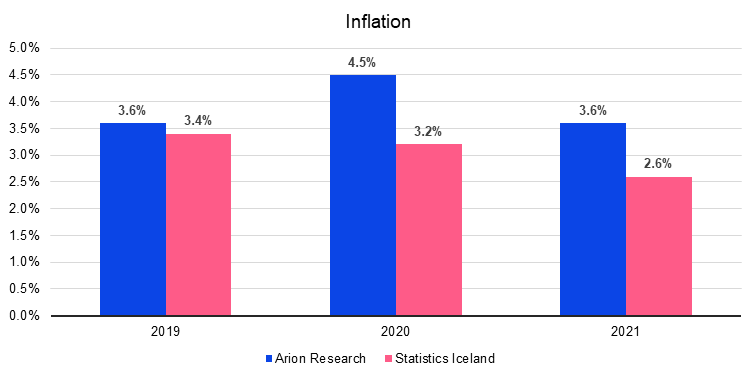

Inflation: There is some difference between the inflation forecasts. Our forecast was published before the signing of collective wage agreements. As the agreements proved to be more prudent than we had dared to hope for, our wage forecast is closer to the ceiling, something that affects the inflation forecast. Our inflation forecast for 2020 is therefore probably too steep, although we feel that Statice is too optimistic. Inflation might lie somewhere between the two forecasts in coming months. However, it should be noted that Statice expects the króna to remain unchanged throughout the forecast horizon, while we expect the króna to depreciate slightly over time.

Sources: Statistics Iceland, Arion Research

Economic Outlook 2020-2023: Every storm runs out of rain

Economic Outlook: Mild winter, cold spring

Tourism in Iceland: Modest angle of attack

Oops, they did it again: Statice revises GDP figures

Wow, 1.4% GDP growth in Q2 without WOW

You shall not pass any further? 25 bps rate cut and silence of the doves

Economic Outlook: Bumpy, but passable

Icelandic tourism fights back

Governor‘s farewell: 25 bps rate cut

Net IIP takes center stage in Q1

The way it was: 1.7% GDP growth in Q1

BoT: Sunshine and showers

Lower rates and dovish tone

Cloudy with a chance of hail according to Statistics Iceland

Economic Outlook: Winter is here

Few options but to keep rates unchanged

The Special Reserve Requirement lowered to 0%

A surprising CA surplus in Q4

Still waiting for a soft landing: 4.9% GDP growth in 2018

Deficit is coming

The doves unsurprisingly win the hawks – unchanged interest rates

The Icelandic Housing Market: Finally levelling off

The Beat Goes On: 2018 in Review

Unchanged interest rates – the króna takes center stage

GDP growth in Q3: Well hello private consumption!

(Almost) a record surplus

Hawkish tone decorated with dove feathers

Economic Outlook: Soft(ish) landing

Tourism in Iceland: Soft landing or a belly flop?

Staggering growth in the second quarter

The surplus shrinks while the external position soars

Balance of trade Q2: The surplus decreases, again

Unchanged interest rates: MPC flexes muscles

Economic Outlook: Summer is Fading

Never Too Old to Learn - Soft Landing Ahead

Strong GDP growth in Q1 not enough to change rates

Current account in Q1: Small, smaller, smallest

Balance of trade in Q1: The incredible shrinking surplus

Similar statements, same interest rates

This is why we expect the króna to depreciate

Winter rates will not let it go

Economic Outlook: Caution, fragile!

Unchanged interest rates, unchanged reserve requirement

3.6% GDP growth in 2017: No cause to change rates

Honey, I shrunk the current account surplus

Trade in services: False alarm?

Unchanged interest rates – No hawks in sight

The Icelandic Housing Market: On the mend

2017 Q4: Icelanders meet expectations, tourists do not

Hurdle on the path to lower interest rates

Economic Outlook: Too good to be true?

Unexpected interest rate cut – Iceland low interest rate country?

Tourism in Iceland: Here to stay?

Private consumption joined the party – 3.4% GDP growth in Q2

Strong króna reduces the current account surplus

Interest rates unchanged – rate cuts put on hold

Economic Outlook: Soft landing ahead?

Payment card turnover increases by 12.2% in June

External trade in a tiny economy

The Central Bank's summer gift: Interest rate cut

Private consumption and external trade fuel 5% economic growth

Five reasons why the Icelandic króna is too strong

Rising sun brings rate cuts

Summary on the Icelandic stock market, dividends and interest in the market

Economic Outlook 2017-2019

Unchanged interest rates – will spring bring rate cuts?

Further steps taken towards capital account liberalization

GDP growth 11.3% in fourth quarter of 2016

Are there grounds for further strengthening of the ISK?

Current account surplus 8% of GDP in 2016

Inflation: Continued tug of war between exchange rate and housing prices

Unchanged interest rates and inflation near target rate

The Icelandic Housing Market: Still in search of equilibrium

The Króna depreciates in the first month of the year

Strong labor market in December and 2016

New majority government formed

Third quarter GDP growth in double digits

Tourists reduce spending amidst appreciating króna

Housing prices keep rising

Allowances to foreign investment of pension funds increased

The times they are a changin’ – parliamentary elections 2016

Arion Research Economic Outlook 2016-2019

Tourism in Iceland: Dreamland or Devil’s Island?