Investor Relations

Macroeconomic updates - all news

Lower rates and dovish tone

The Monetary Policy Committee (MPC) of the Central Bank of Iceland (CBI) has decided to lower the Bank’s key interest rates by 0.5 percentage points, from 4.5% to 4%. The decision is in line with public forecasts, although we were the only one expecting a 50 bps cut. The statement of the MPC was like a box of chocolate, the good kind, full of flavorful and interesting pieces, unsurprisingly perhaps given the economic turmoil of recent months.

After the rough waters of recent months the Icelandic economy has changed course, making a U-turn, as reflected in the CBI’s new macroeconomic forecast. GDP is expected to contract by 0.4%, a significant change from the 1.8% GDP growth forecast published in February, while the inflation outlook is more favorable than before. The króna has treaded water, collective wage agreement has been signed and inflation expectations have become better anchored. All of these factor are mentioned as a rationale for the rate cut. Based on the dovish tone of the statement, the MPC is willing to cut rates even further, perhaps as soon as June. The will and the tools and the threats of rates hike are no more, replaced with the “considerable scope” the monetary policy has to respond to the contraction.

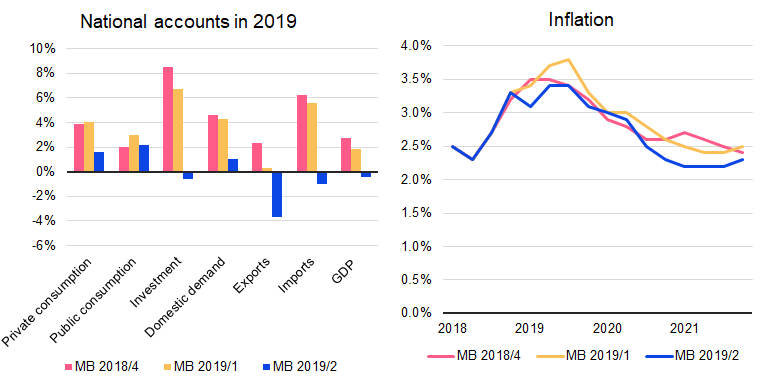

The output gap turns negative

New Monetary Bulletin was published this morning, a publication that we had eagerly anticipated as it included the CBI’s first macroeconomic forecast since WOW air was declared bankrupt. The forecast has changed significantly since February. Instead of 1.8% GDP growth this year, output is expected to contract by 0.4%, a turnaround primarily due to the struggling tourist sector and the capelin catch failure. The hardship of the export sectors is accompanied by a much slower private consumption growth than previously thought, both as a result of rising unemployment and slower purchasing power growth.

The economic downturn means that the positive output gap, which has hitherto been a lion in the path of monetary doves, is rapidly closing and turning into slack in the near future. This is in our opinion one of the most interesting changes in the CBI’s forecast, as the positive output gap has called for tighter monetary stance. Economic slack, coupled with a more favorable inflation outlook, should open up the possibility of further rate cuts in the near future. That being said, we fear that the CBI is underestimating inflation. According to the new forecast, inflation is expected to peak at 3.4% by mid-year, compared to 3.8% peak forecasted in February, despite unit labor cost increases. The change is mainly due to the exchange rate pass-through, which seems to have fallen in recent months. However, it’s not clear if this is a permanent change or if the full impact of the depreciation is yet to be realized. Wage drift is also a concern as wage agreements for the public sector are expiring or recently expired.

Sources: CBI

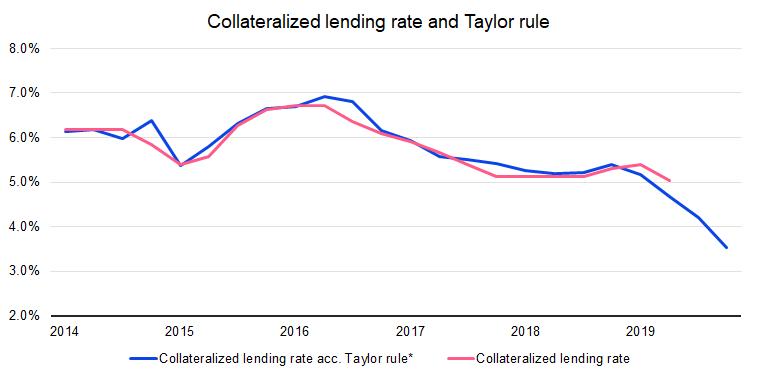

If we plot the Taylor rule, using the CBI’s latest forecast, and the key interest rates together, it’s clear that the MPC at least takes the Taylor rule into consideration when making interest rates decision. The Taylor rule suggests that further rate cuts are underway. The Taylor rule plotted here is based on unchanged interest rates in June. Keep in mind that this is not our official forecast, only a game of numbers. The Taylor rule suggests that there is room for up to 50 bps interest rate cut in June, which, if realized, would push real rates close to zero. As the Governor stated today, real rates close to zero when the economy is contracting is only natural, as long as inflation expectations remain anchored.

Sources: CBI, Arion Research. * Real neutral interest rates are 3% until mid-2015 and get gradually lower thereafter.

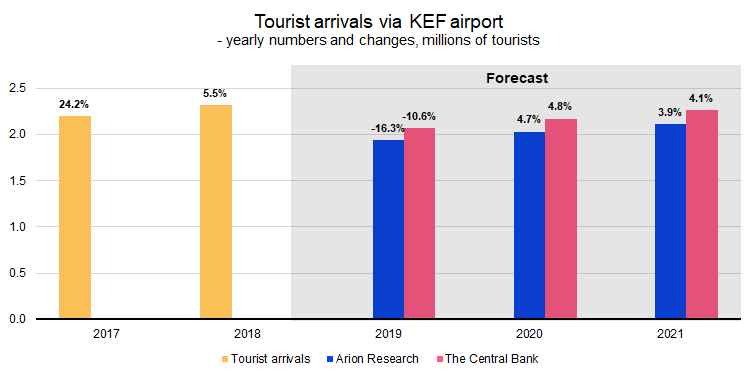

Finally a tourist arrivals forecast from the CBI

Analysts were treated to a surprise today as the CBI finally published a tourist arrival forecast. So far, the Bank hasn’t publicly published a tourist arrival forecast despite it being one of the most important input in the macroeconomic model. We welcome this change, as it makes it easier to understand the inner workings of the CBI’s GDP forecast.

That being said, the CBI estimates that tourist arrivals to Iceland will decrease by 10.5% in 2019. That is somewhat smaller contraction than we assumed in our economic forecast published in late March. According to our estimation tourist arrivals will decrease by 16% this year. Given how Icelandair’s passenger mix has developed over recent months, with the weight of passengers travelling to Iceland increasing considerably at the expense of VIA passengers, our forecast may be too pessimistic. However, that does not mean that we agree with the Central Bank. Year to date, tourist arrivals have decreased by 8% from the same time in 2018. Foreign airlines have to a very limited extent filled the gap which WOW air left behind, at least for the high season, and it is still uncertain when Icelandair’s Boeing MAX aircrafts will take off. For that reason, we believe there is more risk towards the CBI’s alternative scenario which assumes a 15% decline in tourist arrivals this year. The alternative scenario means, other things being equal, considerably larger contraction in exports and a larger economic contraction, or 0.8 percentage points deeper contraction than in the CBI’s baseline forecast. Our Economic Outlook is much more similar to the alternative scenario.

Sources: Icelandic Tourist Board, CBI, Arion Research

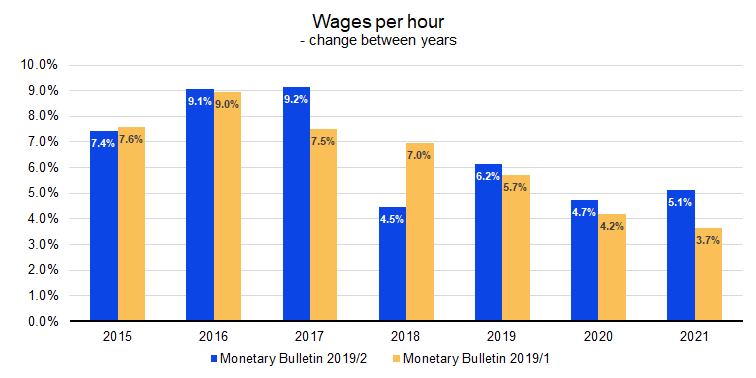

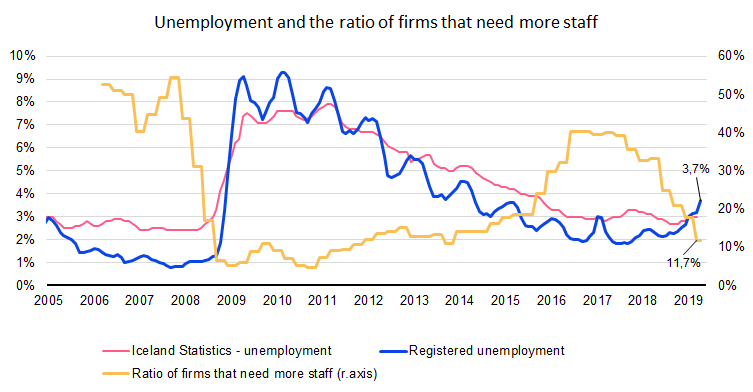

Wage agreements should not threaten price stability

The new collective wage agreements affect the CBI’s forecast of wage developments, but since this year’s raise is rather modest the CBI’s forecast for this year does not change much. Looking ahead to 2021, the CBI now expects wages per hour to increase by over 5%, compared with almost 4% in the last forecast. It is therefore clear that the Bank considers the effect of the collective wage agreements on wage development to be relatively moderate. The main uncertainty factor for this forecast is, of course, the wage drift, but rapidly rising unemployment, along with increasingly fewer companies who consider themselves lacking in staff, should hold it back.

Sources: CBI

Sources: Statice, Gallup, Directorate of Labour Arion Research

There are several mentions in the newly published Monetary Bulletin, that the CBI is concerned about economic development abroad. Economic growth forecasts of the world's major economies have been revised downwards, the interest rate curve in the United States is almost flat, which has often been an indicator of economic contraction, and one of the Bank's scenario assessments is the potential impact of "hard" Brexit on Iceland’s economic growth, inflation, policy rates and other economic variables. Central banks of all major economies are now increasingly more likely to cut rates rather than hiking, which will mitigate partly the effect of lower local rates the interest rates differential, even though long non-indexed rates have declined sharply in Iceland recently.

At the briefing this morning, the Governor stated that foreign central banks have, over the years, been able to fluctuate their real policy rates more than has been the case in Iceland. However, that might have changed although it is too early at this time to say for sure. The words of the Governor may be interpreted as meaning that if inflation expectations remain anchored, the CBI can respond to economic downturns with interest rate cuts that will even lead to a negative policy rate, something that rarely has happened in Icelandic economic history. If the ISK remains stable, the economy contracts, inflation remains within reasonable bounds and inflation expectations remain anchored, we might see, at least temporarily, negative real policy rates.

Economic Outlook 2020-2023: Every storm runs out of rain

Economic Outlook: Mild winter, cold spring

Tourism in Iceland: Modest angle of attack

Oops, they did it again: Statice revises GDP figures

Wow, 1.4% GDP growth in Q2 without WOW

You shall not pass any further? 25 bps rate cut and silence of the doves

Economic Outlook: Bumpy, but passable

Icelandic tourism fights back

Governor‘s farewell: 25 bps rate cut

Net IIP takes center stage in Q1

The way it was: 1.7% GDP growth in Q1

BoT: Sunshine and showers

Lower rates and dovish tone

Cloudy with a chance of hail according to Statistics Iceland

Economic Outlook: Winter is here

Few options but to keep rates unchanged

The Special Reserve Requirement lowered to 0%

A surprising CA surplus in Q4

Still waiting for a soft landing: 4.9% GDP growth in 2018

Deficit is coming

The doves unsurprisingly win the hawks – unchanged interest rates

The Icelandic Housing Market: Finally levelling off

The Beat Goes On: 2018 in Review

Unchanged interest rates – the króna takes center stage

GDP growth in Q3: Well hello private consumption!

(Almost) a record surplus

Hawkish tone decorated with dove feathers

Economic Outlook: Soft(ish) landing

Tourism in Iceland: Soft landing or a belly flop?

Staggering growth in the second quarter

The surplus shrinks while the external position soars

Balance of trade Q2: The surplus decreases, again

Unchanged interest rates: MPC flexes muscles

Economic Outlook: Summer is Fading

Never Too Old to Learn - Soft Landing Ahead

Strong GDP growth in Q1 not enough to change rates

Current account in Q1: Small, smaller, smallest

Balance of trade in Q1: The incredible shrinking surplus

Similar statements, same interest rates

This is why we expect the króna to depreciate

Winter rates will not let it go

Economic Outlook: Caution, fragile!

Unchanged interest rates, unchanged reserve requirement

3.6% GDP growth in 2017: No cause to change rates

Honey, I shrunk the current account surplus

Trade in services: False alarm?

Unchanged interest rates – No hawks in sight

The Icelandic Housing Market: On the mend

2017 Q4: Icelanders meet expectations, tourists do not

Hurdle on the path to lower interest rates

Economic Outlook: Too good to be true?

Unexpected interest rate cut – Iceland low interest rate country?

Tourism in Iceland: Here to stay?

Private consumption joined the party – 3.4% GDP growth in Q2

Strong króna reduces the current account surplus

Interest rates unchanged – rate cuts put on hold

Economic Outlook: Soft landing ahead?

Payment card turnover increases by 12.2% in June

External trade in a tiny economy

The Central Bank's summer gift: Interest rate cut

Private consumption and external trade fuel 5% economic growth

Five reasons why the Icelandic króna is too strong

Rising sun brings rate cuts

Summary on the Icelandic stock market, dividends and interest in the market

Economic Outlook 2017-2019

Unchanged interest rates – will spring bring rate cuts?

Further steps taken towards capital account liberalization

GDP growth 11.3% in fourth quarter of 2016

Are there grounds for further strengthening of the ISK?

Current account surplus 8% of GDP in 2016

Inflation: Continued tug of war between exchange rate and housing prices

Unchanged interest rates and inflation near target rate

The Icelandic Housing Market: Still in search of equilibrium

The Króna depreciates in the first month of the year

Strong labor market in December and 2016

New majority government formed

Third quarter GDP growth in double digits

Tourists reduce spending amidst appreciating króna

Housing prices keep rising

Allowances to foreign investment of pension funds increased

The times they are a changin’ – parliamentary elections 2016

Arion Research Economic Outlook 2016-2019

Tourism in Iceland: Dreamland or Devil’s Island?