Standardizing a "what used to be" a complex process

In 2016, Arion Bank established its Digital Future Accelerator as a means to deliver digitals products to its customer base and respond to current and future competition from banks and FinTech companies. In essence, the accelerator is a 16 weeks project, where employees with the relevant expertise are co-located and their responsibility is to re-engineer a single customer journey. The team of 10-15 people are committed to this single project only during the 16 weeks and leave their daily job. [See in Further reading: Arion Bank Digital Future Accelerator].

Purchasing a place to live is one of the most important decisions people make in their lives. Particularly when it is the first purchase. However, many banks do not make the lending process an easy or a smooth one. It is both time consuming for lenders and at times confusing for those not with financial thinking, may create uncertainty for the seller of the apartment/house if the offer was conditional to financing, and is a costly process for financial institutions due to heavy internal processes.

„We reduced the average processing time of mortgages from 20 days to 5 days for our customers and reduced internal work with 50%“ Höskuldur H. Ólafsson – CEO

It is therefore not surprising that a total redesign of the customer journey of taking a Mortgage and Refinancing of Mortgage was highly prioritized by Arion Bank. The redesign was one of the first projects to go through the Bank’s Digital Future Accelerator.

How much can I afford?

Most future homeowners have a single question before they make a purchasing decision: “How much can I afford to pay?” This usually translates into “Can I afford this particular apartment or house?” In order to answer the question, a bank needs to understand the cash flow (salaries), net wealth status (total debt and equity) and credit score of the purchaser. Fetching this information manually is rarely an enjoyable act for a future purchaser of a new home. Collecting the latest salary slips, last year’s tax return, overview of other loans and assets is burdensome and tedious. Once brought to the bank for review, appropriate documents may be missing or outdated, not adding to the joy of the customer. Additionally, most future homeowners do not secure funding for a new home, but rather the new home. In such a scenario, an offer for the new home is made conditional to financing. That condition creates days or weeks of uncertainty for both the buyer and the seller. On average, this process used to take 10 days.

„Improving the credit assessment process from several days to 3 minutes is convenient banking“ Höskuldur H. Ólafsson– CEO

Simplifying the credit assessment process was therefore an easy decision to make when Arion Bank intended to improve the end-to-end mortgage process. After the customer’s journey redesign, Arion Bank’s customer will have finalized and received their credit assessment in 3 minutes.

Following a positive credit assessment process begins the actual lending process. Before the redesign, customer filled out forms, the Bank’s representatives typed in the information in various systems, presented the loan calculation on paper and needed a written signature on the loan documents themselves. Upon final signature, customers could expect a waiting period of seven days until the loan was paid out to their account of choice.

The Bank’s internal process was very time consuming with several places prone to human error, e.g. typos. Same information was also typed in various systems that were not integrated.

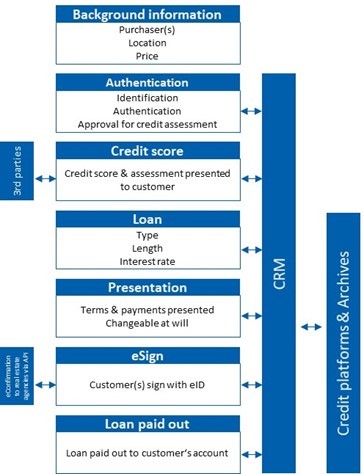

What the re-engineering process entailedOverview of the credit assessment and mortgage process post redesign in Digital Future Accelerator

Redesigning a customer journey starts with the customer. How and what she expects and perceives. Going to the initial drawing board, the Digital Future’s team mapped the current, old process in the first day in the Accelerator and already had a mockup of how the new process should look like on day two. The key premise was always how the customer would flow easily through the credit assessment and lending process without having to gather personal documents herself. Establishing connections to third parties such as the Icelandic Tax Authority (tax return, debt and asset status), eDocument platform (salary slips) and credit score companies were crucial for the credit assessment process. For the lending process, integrating the various systems such as CRM, credit platform, document archives, etc., was the complicated part. The ultimate goal was to have all information and documents flow automatically within and between systems with as little human intervention as possible. With the redesign, time for signing up for an Arion Bank mortgage and having it paid to an account reduced the time for a customer from 15-20 days on average to 5 days. The internal process time at the Bank was reduced by 50% with close to zero risk in documentation error.

Applicable for refinancing as well

Most homeowners have a mortgage. Refinancing a mortgage is therefore a common practice. That means switching financial providers or simply changing the terms, such as type of loan, amortization schedule or deciding on fixed vs. flexible interest rate. Since mortgage refinancing is a highly competitive environment in most markets, it was evident that Arion Bank needed to include the process in its customer journey redesign of mortgages. The same rules of engagement apply for both customer and the Bank, yet they are navigated slightly different through the whole process.

The outcome

The impact has been straightforward in an upward direction. In the first 12 months, volumes of mortgages increased 33% and the NPS (Net Promoter Score) for Arion Bank’s mortgage process went from -2 to +32. During the same period, Arion Bank’s main Icelandic competitors’ mortgage volumes have been more or less stagnant. Over 50% of the Bank’s mortgages are applied for and delivered fully digitally and this number is expected to grow going forward. The number of credit assessments increased with 85% between 2016 and 2017 which means that not only Arion Bank’s customers are using the service. Over 90% of all credit assessments are performed digitally instead of manually. Since the credit assessment is linked to eIDs, which in turn is related to Icelandic social security numbers, anyone with an eID can use the service and use the result to his or her convenience, even with other financial providers. [See further in eID callout box in White Paper: Arion Bank’s Digital Future Accelerator in Further Reading section.]

„The increase in provided mortgages to our retail customers between 2016 and 2017 was 100%“ Bernhard Bernhardsson – Head of Product Development, Retail Banking

Mortgage Applications

All in all, time savings and convenience for customers contribute a great deal to the success of Arion Bank’s Mortgage and Refinancing process. Another factor is privacy. Attending to the Bank’s mortgage process is not limited by banking hours. It can be done in the privacy of one’s home in the evening, which is evidently the most common time of the day when people discuss this important matter. Customers have responded well since going through the first step of apply for a mortgage, credit assessment, is used 45% of the time during weekends and evenings.

Offering an end-to-end digital process also strongly signals to customers the path the Bank is on and shifts customers’ expectations on future communications with the Bank. Some of these expectations may be transferred to other banks in Iceland. For Arion Bank, allowing customers to serve themselves in the privacy of their home in their own time has given more room for engaging conversations with the Bank’s customers when they contact the Bank. Adjusting an important and high impact process on people’s lives in an easy and engaging experience is more convenient banking.

Development of mortgages provided to customers (BISK) Scale intentionally not shown

Digital Credit Assessments

Short demo of user interface for customer‘s credit assessment

Convenient banking is here

Such noticeable change in customer behavior is a strong confirmation of convenient banking. Arion Bank will continue to develop and implement more digital offerings intended to serve its customers better and lower operational costs in the future. As banks will presumably be under stronger pressure to decrease costs in the years to come, Arion Bank has emphasized a combination of better customer experience, intuitive design, decreased cost and new sources of revenue, where applicable. Going forward, shaping a more open banking design with internal and external APIs on top of building expertise in product design such as the credit assessment and mortgages and others, with an end-to-end approach in terms of documentation, is a viable strategy in an ever more competitive environment.

See also description and changes in customer behavior through other Arion Bank’s digital product offerings in the Further reading section below.

About Arion bank

Arion Bank is a leading Icelandic bank offering universal financial services to companies, institutional investors and individuals. These services include corporate and retail banking, investment banking, capital markets services, treasury services, asset management and comprehensive wealth management for private banking clients.

Arion Bank’s balance sheet was more than 1,100 ISK billion (€8.9 billion) in 2017. Arion Bank only has operations in Iceland. Read more about Arion Bank.

Situated in the North Atlantic Ocean between Europe and the United States, Iceland is a European country with 330,000 inhabitants. The capital and largest city is Reykjavik. Two thirds of the country's population live in the Greater Reykjavik area. Iceland, as other Nordic countries, ranks high in economic, political and social stability and equality.

Icelandic citizens are early adopters when it comes to technology and technical infrastructure is good where 97% of residentials have access to internet. Iceland ranked number six globally in terms of GDP per capita in 2016 according to the International Monetary Fund.

Velkomin á vefsíðu Arion banka. Þessi síða notar kökur (e. cookies) til að auðvelda þér að vafra um vefinn, geyma upplýsingar um stillingar o.fl. Sjá skilmála hér.